Comparison Of Health Technology Assessments And Time To Reimbursement For Orphan Drugs And Gene Therapies From Four HTA Agencies

By Steven Kelly, Ioanna Stefani, Nimisha Raj, and Charlotte Poon, Life Sciences Practice, CRA

To encourage manufacturers to invest in the development of orphan drugs (ODs), incentives have been introduced, including research and development grants, tax benefits, accelerated regulatory processes and 10-year market exclusivity. However, ODs and gene therapies (GTxs) still need to overcome a series of challenges posed by national health technology assessment (HTA) bodies, which are unique in each country.

The aim of this study was to review and compare the reimbursement recommendations for ODs issued by four European HTA bodies (France, Germany, England and Scotland) and assess the potential effect of HTA outcomes on the time to reimbursement (T2R). Specific objectives were to:

- Analyze discrepancies in the recommendations from the HTA outcomes of ODs across markets

- Compare T2R and identify which factors contribute to a longer T2R

- Examine a sub-group of GTxs to identify any differences relevant to these innovative products

Methodology

The study reviewed the HTA outcomes and T2R for 80 products that received European Medical Agency (EMA) authorization from 2013 to 2019 and an OD designation at launch. The T2R was calculated from the EMA approval to the date of the negotiated price (Germany and France) or to the date of the National Institute for Health and Care Excellence (NICE) and Scottish Medicine Consortium (SMC) appraisal (England and Scotland, respectively). A comparative analysis was conducted on 71 approved products that were awarded a price in at least one of the four markets in scope. A sub-group analysis was also conducted on five GTxs included in the study (Alofisel, Kymriah, Luxturna, Strimvelis and Yescarta).

Results and Discussion

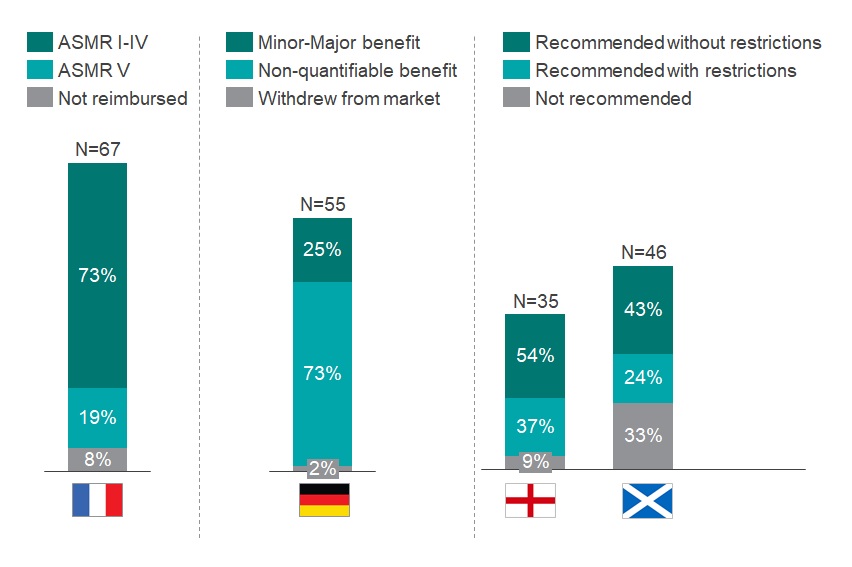

The study found that the rate of recommendation by HTA bodies was highest in Germany, where 98% of the total number of drugs reviewed by the Gemeinsamer Bundesausschuss (G-BA) were approved, compared to 92% reviewed by the Transparency Committee (TC) in France, 91% by NICE in England and 67% by SMC in Scotland. Despite the highest approval rate, 73% of products in Germany were awarded a non-quantifiable benefit, skewed by the automatic additional clinical benefit rating for ODs.1 Conversely, only 19% of the ODs in France were awarded an Amelioration du Service Médical Rendu (ASMR) V, meaning no improvement of medical benefit (Graph 1). The data also suggest that NICE and SMC have a greater tendency to include restrictions beyond the label (37% and 24%, respectively) in order to achieve a positive recommendation. The sub-group analysis identified a similar trend in Germany where three out of the four GTxs assessed by G-BA were awarded a non-quantifiable benefit. Meanwhile, none of these four products was awarded an ASMR V in France. In both Germany and France, Strimvelis was not assessed by HTA bodies but was assessed and recommended by NICE and SMC. Moreover, fewer restrictions were observed in England and Scotland for GTxs, with only Kymriah out of the five GTx products assessed receiving a recommendation with restrictions.

Graph 1: Assessment of HTA outcomes in France, Germany, England and Scotland of all ODs that obtained an EMA approval between 2013-2019. N above each bar equals the number of drugs reviewed by each HTA body.

Source: CRA analysis

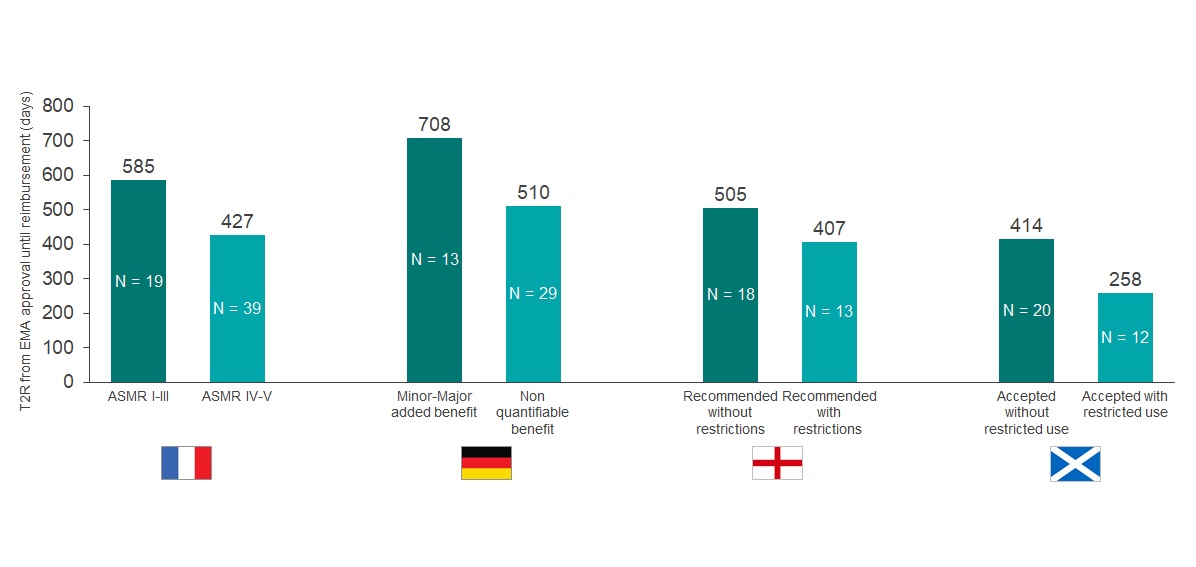

The analysis suggests a correlation between a favorable HTA outcome and a longer T2R (Graph 2). The country with the largest discrepancy is Germany, with the T2R being ~1.4 times longer for drugs with positive ratings (minor to major added benefit), versus products with a non-quantifiable benefit. In France, products with an ASMR IV-V (67% of the products approved) were reimbursed after 427 days on average, versus 585 days for those with an ASMR I-III. Similar trends were also seen in England and Scotland in which the T2R for ODs accepted without restrictions were ~1.2 and 1.6 times longer than those accepted with restrictions, respectively. However, these trends were not fully replicated for GTxs. In France, despite receiving an ASMR III rating, both Kymriah and Yescarta were reimbursed ~1.6 times quicker than Alofisel (ASMR IV), running counter to the trend observed in the full analysis. In England, the average T2R for GTxs recommended without restrictions was about three times longer than those with restrictions. Except for Kymriah, T2R in Germany was not calculable for GTxs as they were still within the free pricing year at the time of the analysis.

Graph 2: Comparison of T2R (days) for EMA ODs approved from 2013-2019. ODs were reimbursed in at least one of the selected markets (N = 71). N within each bar equals the number of drugs with each outcome reviewed by each HTA body.

Source: CRA analysis

In France, our findings suggest that a temporary authorization for use (ATU), which enables early access to new treatments, may correlate with a longer T2R for ODs. The average T2R for ODs launched with and without an ATU in 2018 was 251 and 122 days, respectively. This is consistent with the 2018 annual report of the Pricing Negotiations Committee (CEPS) and may be due to the lower incentive for manufacturers to expedite the price negotiation if a product is already available in the market.2,3 However, the analysis on GTxs suggested that the opposite was true. Kymriah and Yescarta were granted an ATU and were reimbursed ~1.6x faster than Alofisel (without an ATU).

In England, although the highly specialized technology (HST) pathway supports broader criteria for the cost-benefit assessment of ultra-orphan drugs and a higher cost per quality-adjusted life year (QALY), our data showed that HST does not speed up T2R (494 days with HST versus 470 days with a single technology appraisal [STA]). A more pronounced discrepancy was observed in GTxs, where T2R was 472 days through HST versus 137 days through STA. Furthermore, inclusion of a patient access scheme (PAS) was consistent with a longer T2R in England, (523 days versus 311 for products with [N=25] and without [N=7] a PAS). The same observation applied to GTxs. Luxturna was recommended with a PAS and reimbursed after 322 days, while Kymriah and Yescarta (both without a PAS) were reimbursed after just 121 and 153 days, respectively.

Conclusion

Despite several concessions to support better outcomes for ODs, we found that reimbursement assessments are inconsistent across the EU markets included in the study. Although Germany had the highest OD approval rate (98%), this was achieved predominantly (73%) with an unquantifiable benefit. A more favorable outcome from G-BA took on average 1.4 times longer to achieve a negotiated price (708 versus 510 days). While France and England had comparable approval rates (92% and 91%); the TC in France reviewed almost twice the number of ODs over the same period of time (67 versus 35 drugs). A high proportion (67%) achieved an ASMR IV-V, suggesting that reimbursement was achieved at a lower value but more quickly than products with an ASMR I-III (427 days versus 585 days).

In England, 37% of ODs appraised by NICE achieved approval in a restricted population versus the EMA label and accepting such restrictions enabled faster appraisal time (407 versus 505 days). Although introducing a PAS improved the chance of approval, our analysis also suggests it delays the overall appraisal time (523 versus 311 days). The highest rate of non-approval was observed in Scotland, where 33% of drugs reviewed by the SMC were not accepted although a third of these were due to lack of manufacturer submission.

The sub-group analysis on GTxs identified a handful of exceptions in France and England. In France, Kymriah and Yescarta achieved early access and ASMR III which, contrary to our predictions from the full analysis, yielded a shorter T2R. In England, it was notable that GTxs were assessed much quicker through the STA process than either the HST process or the STA process for ODs. Interestingly, the two GTx products assessed through the STA process were Kymriah and Yescarta and the rapid approval could be due to the preparedness of NICE, where a prior mock assessment had demonstrated that the products were likely to be cost-effective.4

Overall, concessions introduced in the HTA process for ODs have a positive impact on minimizing rejections and accelerating the T2R. However, obstacles remain to capture the full value of ODs and GTxs within the HTA process. Achieving more favorable outcome ratings, avoiding restrictions, or addressing uncertainty with a PAS all lead to prolonged appraisal times. Manufacturers are therefore still required to carefully consider their launch strategy and further flexibility to address uncertainty in the HTA processes is needed to improve reimbursement timelines and outcomes for ODs and GTxs.

The views expressed herein are the authors and not those of Charles River Associates (CRA) or any of the organizations with which the authors are affiliated.

REFERENCES

- Bouslouk M. G-BA benefit assessment of new orphan drugs in Germany: the first five years. (2016): 453-455.

- CEPS Comité économique des produits de santé. Rapport d’activité 2018. November 2019.

- Ministère des Solidarités et de la Santé. Rapport sur la réforme des modalités d’évaluation des medicaments. (2015).

- Office of Health Economics. Exploring the Assessment and Appraisal of Regenerative Medicines and Cell Therapy Products: Is the NICE Approach Fit for Purpose? February 2017.

ABOUT THE AUTHORS

Steven Kelly is a Vice President at CRA with more than 20 years of experience working in health technology assessment, evidence-based medicine, health economics, and pricing and market access within the pharmaceutical industry. He joined CRA in 2018 and has worked on a broad range of therapeutic areas throughout the lifecycle.

Ioanna Stefani is a Senior Associate at CRA with over 5 years’ experience in pricing and market access strategy in the life sciences industry. Her areas of expertise include launch readiness, innovative contracting and portfolio strategy projects specifically in haematology, oncology, and orphan and autoimmune diseases.

Nimisha Raj is a Consulting Associate in the Life Sciences Practice at CRA. Over recent years, she has worked on several strategic consulting projects for leading pharmaceutical and biotechnology companies, focusing on pricing and market access in Europe.

Charlotte Poon is an Associate in the Life Sciences practice at CRA. She has worked on a range of projects for leading pharmaceutical and biotechnology companies and trade associations, focusing on complex strategic and policy challenges in the life sciences industry.